No doubt you’ve heard that mortgage rates are low. They’re lower than they’ve ever been in history. The news is everywhere.

Just check out some of these headlines from the last 24 hours:

- Mortgage rates set new lows for the 6th straight week (Reuters)

- Mortgage rates fall again; 30-year fixed at 4.54% (Wall Street Journal)

- Mortgage rates hit another low : 4.54% (NPR)

Fixed mortgage rates are now down more than 1/2 percent from the start of the year, and 3/4 percent from just 1 year ago. The drop has dramatically improved home affordability for home buyers while creating refinance opportunities for existing homeowners.

From a payment perspective, a conforming, 30-year fixed rate mortgage is now cheaper by $41.94 per month per $100,000 borrowed versus July 2009.

A homeowner with a $300,000 mortgage, therefore, is saving $45,295.20 over 30 years.

Low mortgage rates rarely last long and rates appear to have troughed. After a big downhill between April and July, they’re now flat. This could mean rates have finished falling, or that they’re gearing up for another drop lower. Either way, if you haven’t talked to your real estate agent about home affordability, or us about refinancing, it may be time to make that call.

If today’s market marks the end of low rates, rates are expected to rise quickly.

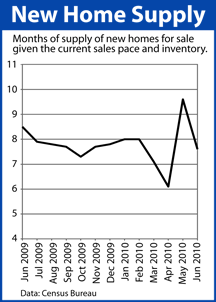

The Pending Home Sales Index plunged in May 2010, just one month after the expiration of the federal home buyer tax credit program.

The Pending Home Sales Index plunged in May 2010, just one month after the expiration of the federal home buyer tax credit program.